Product Description

Customers answer questions about health and lifestyle.

Then we help you figure a best estimate of the cost of living for the years of the term.

You can organize costs by year, child, and category.

You can choose either Single Premium or Level Pay (Annual).

So how does it work?

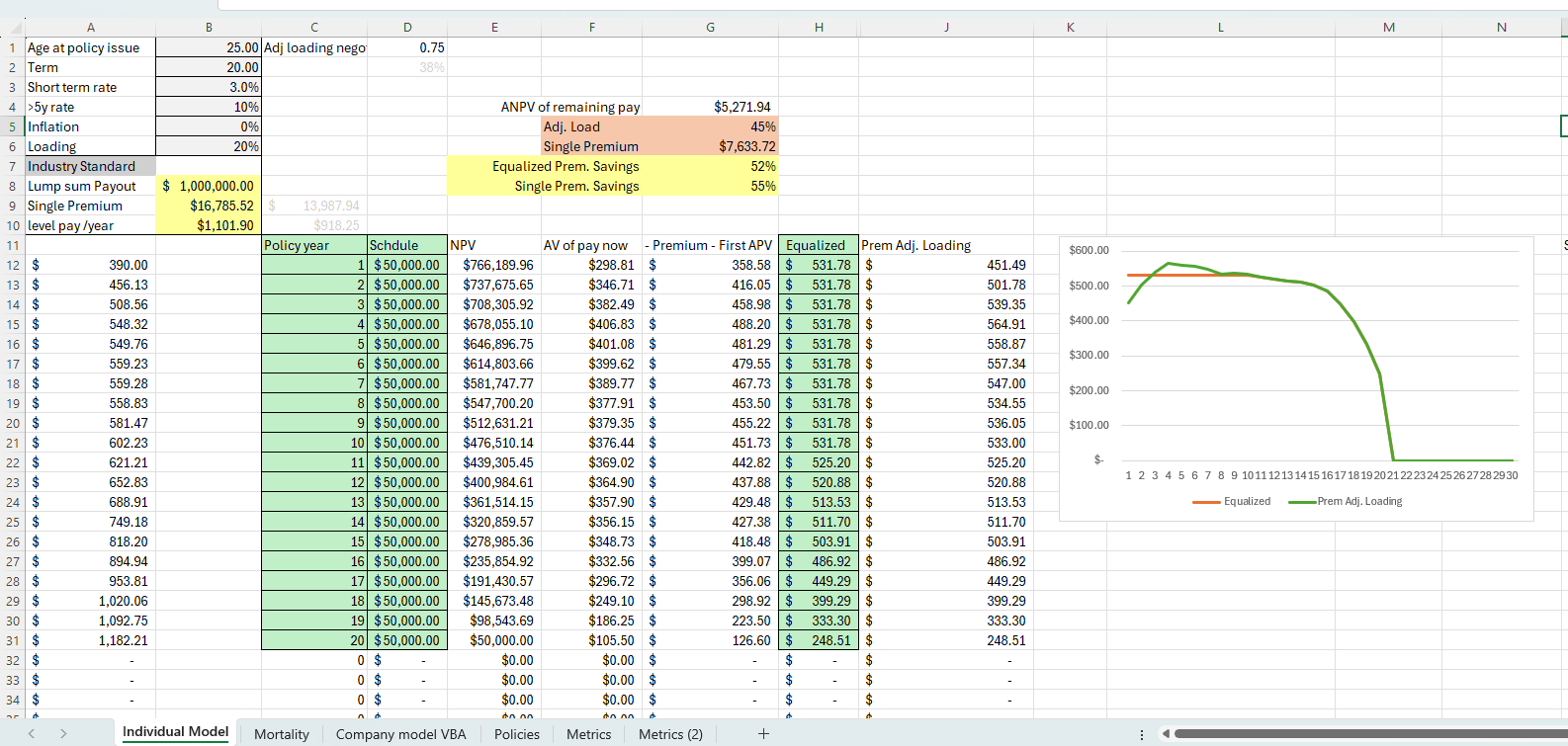

Let's say Joe Insured dies in the 3rd year of a 20 year term.

Joe's family (beneficiaries) will get the money in the 3rd year bucket.

At the beginning of Year 4, they will get Year 4's amount. And for Year 5 at the beginning of Year 5. etc.

Optional Riders

Final Expenses: Those don't decrease over time.

Be covered for the same amount for the life of the policy.

Gauranteed Purchase Option: Extend your term when you have a more children without new underwriting.

Milestones: Keep Wedding money available for years.

We don't know when each person find his soul-mate.